Overview

Apart from the gaining urgency of Brexit negotiations, the Eurozone

has been the stage for another unfurling political crisis earlier this year. The Italian general election, held in March 2018, has given voice to the country's unhappiness with EU's fiscal rules, banking regulations and trade deals, which are being held responsible for stifling Italy's response to weak economic growth and increased immigration.

Campaigning by its two leading parties, the anti-establishment Five Star Movement and the far-right League - who have now formed a coalition government - focused on revitalizing Italy's economy through a series of tax cuts and increases in public spending.

The political uncertainty leading up to the coalition government,

the turning of a previously pro-European Union (EU) country into

a Eurosceptic voice, and the anticipated rise in Italy's already high national debt, have all shaken up the country's bond and equity markets. At its lowest point on May 29, 2018, the yields on two-year Italian debt touched a five-year high of 2.73 percent, while the 10-year debt touched 3.388 percent.

WNS DecisionPoint analyzed the Italian political crisis for its impact on its sovereign debt, with specific focus on risk exposures of European financial institutions. Some of the key findings include:

- Although bond prices have firmed up in June, yields are still higher than pre-selloff levels, indicating an added risk premium of around 0.8 percent to Italian debt

- Italian debt sales have suffered from the political upheaval, with syndicated debt sales lower by 42 percent year-on-year

- Bank of Italy's Intra-Eurosystem liabilities have gone up by over

16 Billion euros in the one month between May and June 2018, driven by an exodus of consumer and bank deposits to other EU banks

- With Italian, Spanish, German, Belgian and French lenders heavily exposed to Italian debt, the cost of insuring European banks against default has gone up

This report assesses each finding to trace immediate and medium-term impact on Italian and Eurozone banks.

Introduction

After months of political turmoil following the March general election with no political party securing an absolute majority,

the anti-establishment Five Star Movement and the far-right League agreed to strike a deal to govern together. The two parties proposed the name of Giuseppe Conte, a civil lawyer and academic, as the country's new prime minister to lead their populist government. Five Star and the League have pledged to reshape the Italian economy through a mix of tax cuts and spending increases that risk increasing the budget deficit, in defiance of the EU rules. They have also challenged the EU trade deals and sanctions against Russia. While political stability was restored following the formation of the coalition government, the run-up to this ending was marred by several turn of events that took a toll on the Italian financial markets and has left a question mark on the future of Italian politics and Italy's membership of the EU.

ELECTIONS AND SUBSEQUENT GOVERNMENT FORMATION

The anti-establishment Five Star Movement and the far-right League were winners in the March 2018 elections, but their gains were not decisive enough to enable them to govern single-handedly. As a coalition, they have a small majority in parliament.1 Both the parties held on-off talks about forming a coalition alliance for weeks following the indecisive outcome of the general election in March. However, they came close to striking a deal on May 10, 2018.

Luigi Di Maio, head of Five Star, and Matteo Salvini, the League leader, discussed the agenda and policies of a joint government, as well as choices for prime minister and cabinet positions.

Alliance between Five Star and the League has been viewed as the most destabilizing election outcome for the eurozone since both parties have openly voiced their criticism of EU fiscal rules, banking regulations and trade deals.

A few days prior to these coalition talks, Five Star and League had settled on a second election this year, which would have been unprecedented in Italy's history, as the only way to break the stalemate.2 However, a breakthrough came when Silvio Berlusconi, the former prime minister and media mogul close to Salvini, gave his support to

the formation of a coalition.3

WHERE THE TWO PARTIES STAND ON MAIN POLICY ISSUES?

After a campaign dominated by promises to revitalize the economy and defend Italian interests in the wake of Brussels' dominance, the two populist parties succeeded in securing power. However, given the parties' disdain for eurozone policies, the attention will now turn to how destabilizing will be the impact of their policies on the Italian economy and the larger eurozone politics.

Financial Market Response and the Turmoil Thereafter

The Italian financial markets entered a period of continuous mayhem. Failed coalition talks, a political novice taking charge of the new government and appointment of a Eurosceptic finance minister and subsequent opposition of the Italian president, Sergio Mattarella, created unexpected twists and turns in the Italian bond and equity markets, with the ripple effect being felt in markets across Asia and the U.S. In the next sections, we track the movements of Italian bonds and equities in the aftermath of numerous political events.

MAY 16, 2018: ITALIAN BOND SELL-OFF AFTER REPORTS EMERGED OF A COALITION GOVERNMENT BETWEEN POPULIST PARTIES

Italian bond prices fell sharply on May 16, 2018, propelling the benchmark 10-year yield beyond two percent and to its highest level in two months after reports emerged that the two populist parties were set to form a coalition government that would break away from economic orthodoxy.4 Bond prices and yield move in opposite directions, with a higher yield reflecting the higher risk premium attached to the government bond. Government bonds with high risk premium denote the prospects of the government defaulting on its debt in light of political certainty and unconventional fiscal policies of the two populist parties.

ITALY'S 10-YEAR GOVERNMENT BOND YIELD TILL MAY 16, 2018

The yield on the Italian 10-year bonds rose by 13 basis points to 2.08 percent, its biggest daily rise since June 2017. The gap between 10-year German and Italian bond yields - a widely-watched indicator of eurozone political stress - rose to 144 basis points, up from 129 on May 15, 2018, and to its highest level since the Italian election in March. Milan's stock market also suffered; the FTSE MIB fell 2.3 percent.5

MAY 21, 2018: ITALIAN BOND MARKETS HIT HARD AFTER GIUSEPPE CONTE'S NAME IS PROPOSED FOR PM

The hectic trading volumes on Italian debt and equity markets continued as investors reacted to the possibility of anti-euro parties taking power in Italy. The key factor in the political mess has been the

market, as it waits to see the direction the two Eurosceptic parties take with regard to Italy-Brussels relations and fiscal policies. The 10-year bond yields rose 20 basis points to 2.42 percent, taking its total rise in the past weeks to 64 basis points. The premium over German debt hit 189 basis points, its highest level since June 2017.6

ITALY'S 10-YEAR GOVERNMENT BOND YIELD TILL MAY 21, 2018

Milan was one of Europe's most active equities market with more than 4.5 Billion euros of Italy-listed shares trading, according to data from Cboe Global Markets Europe.7 After opening more than 2 percent lower, the market pared losses and closed with a drop of 1.5 percent, in the process slipping behind France's CAC 40 as the best performing European equity benchmark for 2018. Investors sold bank stocks, which are highly exposed to Italian sovereign bonds, as uncertainty emerging from a coalition deal between two parties with anti-euro ideology wreaked havoc in the markets.

MAY 29, 2018: ITALIAN BONDS WITNESSED HEAVY SELLING AFTER THE COUNTRY'S PRESIDENT, SERGIO MATTARELLA, FRUSTRATED A BID BY THE TWO POPULIST PARTIES TO FORM A COALITION GOVERNMENT

Italy's bond market suffered a steep slide, resulting in the highest ever yields reached by the country's two-year bond in more than four years. The yield on the two-year Italian debt broke through 2.7 percent for the first time since 2013, reaching as high as 2.73 percent - up nearly 2 percentage points from the close of markets. The yield on 10-year debt hit 3.388 percent, up from 70 basis points from previous close.8

Investors sold Italy's bond and equities after the country's president, Sergio Mattarella, frustrated a bid by the Five Star Movement and the League to form a coalition government. This led to a fear amongst investors that this move could be a trigger for fresh elections that might give a more definitive Eurosceptic mandate to the two populist parties.9

The bid to form the government was dropped after Mr. Mattarella blocked the nomination of an explicitly Eurosceptic finance minister, Paolo Savona, in a dramatic stand-off. The president, who has the power to approve or block cabinet appointments, considered the appointment of Mr. Savona as a threat to Italy's membership of the eurozone.

As a sign of negative investor sentiment, the gap in yield between Italy's 10-year bond and German Bunds of the same maturity, a key measure of perceived risk of Italian bonds, climbed to 314 basis points, up from 234 basis points. The weakness in Italian markets fed through into other eurozone periphery nations' debt yields. The 10-year Portuguese yield rose by 31 basis points while the Spanish yields witnessed a move by 14 basis points.10

JUNE 1, 2018: ITALIAN 2-YEAR BONDS STAGED DRAMATIC PICK-UP AFTER PRESIDENT APPROVED THE NEW GOVERNMENT

After almost 90 days of elections, Italian bond prices recovered from their painfully low levels when the League and Five Star Movement secured the approval of the president to forge a coalition government after striking a last-minute deal. The country's two-year yield dropped 36.2 basis points to 0.814 percent on the heels of an 81.2 basis points drop in the previous session.11 Yield on the two-year bond had taken a jump over concerns that a fresh slate of elections would become a referendum on Italy's membership of the eurozone.

Investors also bid up Italy's 10-year Business Transaction Protocol (BTP) on the day, sending the yield lower by 16 basis points to 2.677 percent, below the highs above 3 percent that were hit earlier. The easing brought down the gap between the Italian 10-year BTP and German Bunds with the same maturity to 231 basis points from the peaks of 283 basis points.12

Outflows from European funds also accelerated sharply, as investors were unnerved over Italy's uncertain political future, exposing them to the region's stormy financial markets. Western Europe-focused equity funds suffered USD 4.5 Billion of outflows for the week ending May 30, according to data from EPFR Global.13

ITALIAN BONDS: SHAPE OF THE YIELD PATH

The path of Italy's bond yields is a demonstration of the roller-coaster ride the financial markets have been on in the last several weeks. A month after investors reacted with panic to the formation of

an anti-euro establishment at the center by accelerating a sell-off, Italian debt has settled at new levels.

The Italian two-year bond, which

was the focus of much of May's price moves, yielded around

0.9 percent in June, down from

1.1 percent seen in the second week of June and well off the high of 2.731 percent it hit at the peak of the crisis.14 The 10-year bond yield has been pulled up in its wake, hitting 3.388 percent before settling back into a range of between 2.5 and 3 percent.15 Two-year yields seem to have settled at 0.6 percent and have been unable to get below this mark, which now seems to be the new floor price. Given that the two-year bond was yielding -0.2 percent before the sell-off, it suggests that a new risk premium of 0.8 percent has been attached to the Italian assets' yields.16

Italian Debt sales suffered from the political shock

The Italian debt experienced a decline in sale value as the political upheaval of May and June startled investors. Before investors were petrified by the Italian election outcome, an auction of 12-month debt yielded -0.361 percent,17 implying that investors were willing to endure a minor nominal loss to hold the paper to maturity. An auction of 6 Billion euros in debt held in the second week

of June came with a yield of

0.55 percent,18 the highest the 12-month paper saw in four years. The deal signifies that investors want to be better compensated for the risk they are taking on by investing in Italian debt.

A similar scenario was seen in the auctions of 5-year, 7-year and the 10-year Italian debt. The auction held in the last week of June saw 2 Billion euros of the five-year paper collect a yield of 1.82 percent, half a percentage point less than similar sales conducted in May.19 The 7-year paper fetched a yield of 1.67 percent and the 10-year paper yielded 2.77 percent. It is worth noting that all these yields are much higher than those seen at the eurozone pre-crisis levels.20 According to data provider Dealogic, Italian borrowers have sold 45 Billion euros worth of syndicated bonds since the start of 2018, 36 percent lower than the amount sold during the same period last year.21

According to Dealogic, Italian corporate debt sales have declined by 45 percent year-on-year, while Italian financial institutions have sold 21 percent less debt in comparison to that sold in the first half of 2017. Syndicated debt sales by the Italian government, agencies and supranationals have declined by 42 percent year-on-year.22

IMPACT ON THE BANK OF ITALY'S BALANCE SHEET

While investors and the Italian bond market were the primary victims of the political chaos of last month, the Bank of Italy also bore the brunt of the

uncertainty inflicted by the general election. WNS DecisionPointTM calculated the month-on-month changes in the Bank of Italy's balance sheet for May-June 2018 to assess the impact of the turbulence on the key assets and liabilities of the Bank of Italy.

The Bank of Italy's Trans-European Automated Real-time Gross Settlement Express Transfer System (Target 2) liabilities, highlighted in bold, rose by

39 Billion euros during the peak of the May crisis, and declined slightly by 16 Billion euros in June, driven by an increase in the central bank's liabilities to the commercial banks. This means Italian banks have pulled assets out of the central bank and deposited them across the Eurosystem's banking institutions.

One of the main driving forces for this could be a reduction in outstanding deposits of customers in Italian banks. Italian customers could have wired a part of their deposits to other accounts in banks in different euro area countries. Customers could also have used their deposits to buy financial securities sold by residents of other euro area countries. All of this indicates a distrust of Italian banks, with an intent to reduce exposure to Italian assets and securities and a preference for foreign bank accounts or financial assets.23 The main trigger behind the series of events is the redenomination risk, wherein a country's currency is recalibrated due to high inflation, a currency union formation or a currency union break-up.24

The Eurozone banking system and the Insurance market were not spared either

The political crisis of Italy brought the theory of 'doom loop' in the banking system back in focus. Doom loop is the phenomenon wherein poor

performing banks can destabilize a country's government and heavily-indebted governments can push banks holding their bonds over the cliff.

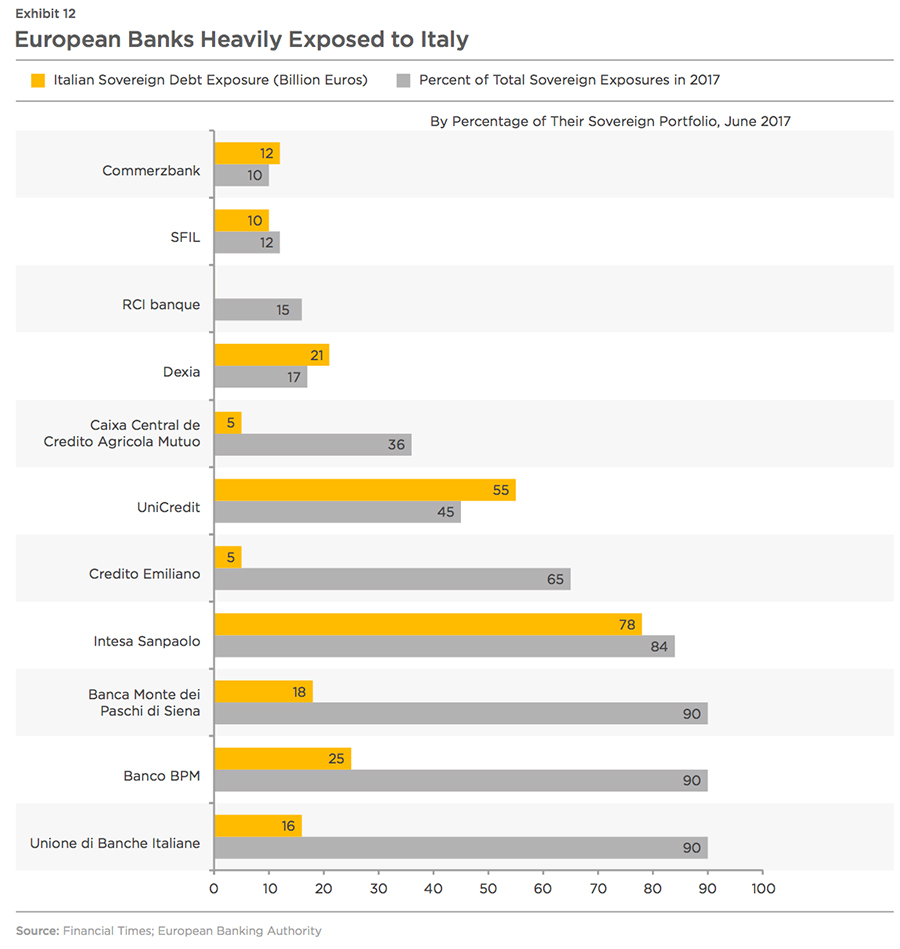

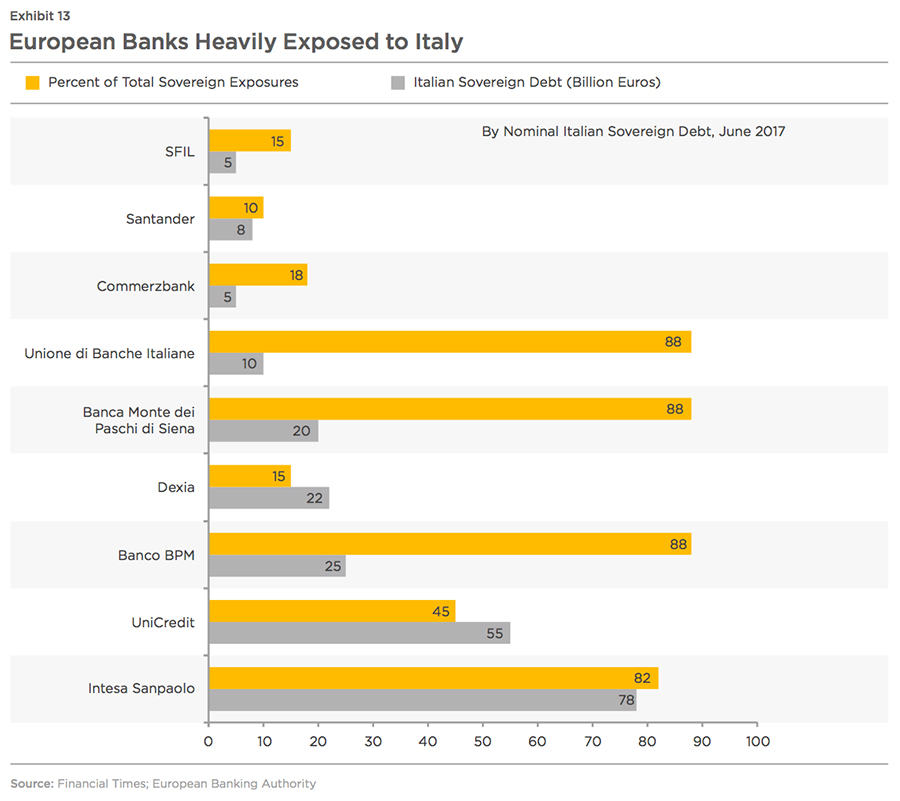

Italy has one of the highest debt levels in the world at more than 130 percent of GDP. Italy's banks are heavily exposed, with Italian sovereign bonds accounting for almost 10 percent of assets at the end of last year, according to Bank of Italy.25 This is a higher proportion than most other European countries. Italy's biggest lending institutions have the highest overall exposure to the country's sovereign debt: Intesa Sanpaolo had 76 Billion euros at the end of 2017 and UniCredit had 54.5 Billion euros.26 In both cases, their exposure exceeded the size of their capital buffers, highlighting what is at stake.

Banca Montei dei Paschi di Siena's exposure to its own government made up more than 90 percent of the 21.7 Billion euros of sovereign debt held by the recently bailed-out bank at the end of June 2017, according to the European Banking Authority. The fall in the shares of Italy's three largest banks can be attributed to this.27 Spanish, German, Belgian and French lenders are also heavily exposed to Italian sovereign debt. Belgium's Dexia had 22 Billion euros of such exposure at the end of 2017, a reflection of the state-owned bank's legacy business of public sector finance. Germany's Commerzbank had 9 Billion euros. In Spain, Banco Sabadell had 10.5 Billion euros in June 2017, while BBVA had 9.6 Billion euros and Banco Santander had

8.8 Billion euros.28

France's BNP Paribas had

9.8 Billion euros of Italian sovereign debt at the end of last year, a legacy of its acquisition of Italy's BNL more than a decade ago. French rivals, BPCE and Credit Agricole, which have significant investments in Italy, had 8.5 Billion euros and 7.6 Billion euros of exposure respectively.29

European insurers are also on the edge. Italy's Generali is the insurer with by far the maximum exposure to Italian government bonds and shareholder exposure standing at 92 percent of tangible book value.30

THE PRICE OF INSURING EUROPEAN BANKS AGAINST DEFAULT HAS SOARED

The cost of insuring against default by European banks shot up, as the iTraxx senior financials index produced by Markit rose more than 50 percent to reach its highest level for more than a year.31

While the crisis has increased funding costs for banks, it has also

dashed hopes of the European Central Bank raising interest rates from their current negative levels, which have been squeezing banks' profit margins.32 Italian banks will benefit from the higher sovereign bond yields in the short term, in which they invest majority of their cash from depositors. However, the crisis has also stalled the progress made in reducing the amount of non-performing loans, which account for more than 10 percent of their total loan books.33

Conclusion

Italy's political and economic future is set for a roller-coaster ride in the coming months, with the new populist coalition government ready to announce its autumn budget. The expectation is that the new government will stick to its respective campaign promises,

launching ambitious fiscal stimulus programs and pension schemes.

However, a strong opposition to the government's budget proposals in Brussels, along with internal disagreements in the coalition could be a trigger for fresh

elections in Italy in the coming months. Fresh elections in Italy could ultimately take the form of a referendum on Italy's future in the eurozone, something that the financial markets would not like to see.

References:

1. Article by Financial Times, 'Italy's populist parties edge closer to deal to govern', May 2018

2. Ibid

3. Ibid

4. Article by Financial Times, 'Italian bonds wobble on political fears', May 2018

5. Ibid

6. Article by Financial Times, 'Italian bonds hit hard by political risk over new government', May 2018

7. Ibid

8. Article by Financial Times, 'Italian bonds suffer rout on political turmoil', May 2018

9. Ibid

10. Ibid

11. Article by Financial Times, 'Italian bonds rally sharply after president approves new government', June 2018

12. Ibid

13.Article by Financial Times, 'Italy turmoil accelerates outflows from Europe', June 2018

14. Article by Financial Times, 'Italian Bond Yields: Wave formation?', June 2018

15. Ibid

16. Ibid

17. Article by Financial Times, 'Italy pays up in short-term debt sale', June 2018

18. Ibid

19. Article by Financial Times, 'Italian debt sale confirms political risk premium', June 2018 20. Ibid

20. Ibid

21. Ibid

22. Article by Financial Times, 'Italian debt sales fall as political tensions linger', June 2018

23. Article by Financial Times, 'The monetary aftermath of Italy's chaotic month', June 2018

24. ECB Europa

25. Article by Financial Times, 'Italy turmoil shows banking 'doom loop' still a powerful force', June 2018

26. Ibid

27. Ibid

28. Ibid

29. Ibid

30. Ibid

31. Ibid

32. Ibid

33. Ibid