Overview

The challenges posed by the global financial crisis in the recent past has compelled financial institutions to consider non-conventional methods. One such intervention is the European Central Bank's (ECB) Asset Purchase Program (APP).

Through the program, the ECB purchases a range of assets such as government bonds, corporate bonds and covered bonds, enabling it to influence the overall macroeconomic stability. Asset purchase triggers a price increase in private sector assets which further catalyzes the reduction in loans and lending rates for households and businesses. The APP also helps create dispensable funds for investors in return for assets sold to ECB. These funds get invested into other assets within or outside the Euro market, resulting in reduced borrowing rates in capital markets or boost in inflation, respectively. In 2017, ECB's total assets was EUR 414.2 Billion on account of purchases of securities under the APP.

In an October 2018 survey by ECB, when asked about the impact of APP, Euro area banks reported an overall negative impact on their profitability over the previous six months. A small percentage of banks also reported that the APP had contributed to a decline in capital ratios in the previous

six months.

While there has not been any visible impact on profitability, banks still perceive future challenges to their operations once the APP ends, specifically with regard to loan loss provisions. Banks, thus, consider APP as detrimental to their operations.

In this paper, WNS DecisionPoint takes a closer look at the data and metrices to assess the real impact of APP on banks. It analyzes the key indicators of banks' total profits such as operating profit and total profit before tax; and dives into key variables such as the lending deposit spread

across the duration of the program.

As the curtain draws on the APP in 2018, ECB needs to evaluate how well it could achieve its goals in the macroeconomic context and how it plans to continue enabling long-term gains for banks in the region.

ASSESSING THE IMPACT OF ASSET PURCHASE PROGRAM ON EURO REGION BANKS

IS THE EUROPEAN CENTRAL BANK'S GAMBIT PAYING OFF?

- The European Central Bank (ECB) buys a

range of government and private assets under the Asset Purchase Program (APP) to influence broader financial conditions and economic growth

- In June 2018, ECB's governing council

announced the reduction of the monthly net average purchase pace to EUR 15 Billion till December 2018, as against the average of EUR 30 Billion across 2018 and EUR 60-80 Billion across different periods between 2015 and 2017

- The overall impact of APP on bank

profitability has been varied. There are positive effects as a result of scarcity created by increasing capital gains and pace of credit offtake; the negative effect on profits is on account of narrowing lending-deposit rate spread

NEED FOR AN ASSET PURCHASE

PROGRAM

Under normal economic conditions,

the European Central Bank (ECB) steers the monetary policy and broader financial conditions by setting the short-term key interest rates. However, the global financial crisis of recent years has forced central banks to adopt non-conventional measures to drive macroeconomic stability. Key interest rates have come to their lower bound - a point at which lowering them further willhave no impact. The ECB turned to less conventional methods to ward off the risks during a period of low inflation lasting for too long, and to bring inflation back to levels below 2 percent over the medium term.1 Asset purchases are one of the non-standard measures of achieving this.

WORKING OF THE ASSET PURCHASE PROGRAM

Under the expanded Asset

Purchase Program (APP), the ECB buys a range of assets, including government bonds, securities issued by European supranational institutions, corporate bonds, asset-backed securities and covered bonds at a rate of EUR 30 Billion per month.2 financial conditions and eventually impact growth through three main channels:

Direct Pass-through

The ECB drives up the value of

private sector assets such as assetbacked securities and covered bonds, which are linked to loans that banks grant to households and firms, by buying them and thereby increasing their demand. This spurs banks to make more loans, which they can then use to create and sell more asset-backed securities or covered bonds. The increased supply of loans tends to lower bank lending rates for companies and households, improving broader financial conditions.3

Portfolio Rebalancing

The ECB purchases private and

public sector assets from entities such as banks, households and pension funds. The funds the investors receive in exchange for

the assets sold to the ECB can then be invested in other assets. By increasing demand for other assets, this process of portfolio rebalancing leads to an increase in prices and lowering of yields, even for assets not directly engaged under the APP. This reduces the borrowing costs for companies seeking to obtain financing in the capital markets. Also, the lower yields on securities encourages banks to lend to companies or households. The increased supply of bank lending to the real economy lowers the borrowing costs for households and firms. If, on the other hand, investors use the funds to buy higher-yielding assets outside the euro area, this may also lead to a lower euro exchange rate and hence boost inflation.

Both the direct pass-through

and portfolio rebalancing channel improve broader financial conditions in the eurozone. By lowering borrowing costs, asset purchases stimulate investment and consumption.

Signaling Effect

Asset purchases signal to the market that interest will remain low for a certain period of time. This helps to reduce uncertainty and volatility in the market regarding future interest rate developments. They also serve as a guiding factor in the market with regard to the path of interest

rate movements and future investment decisions.

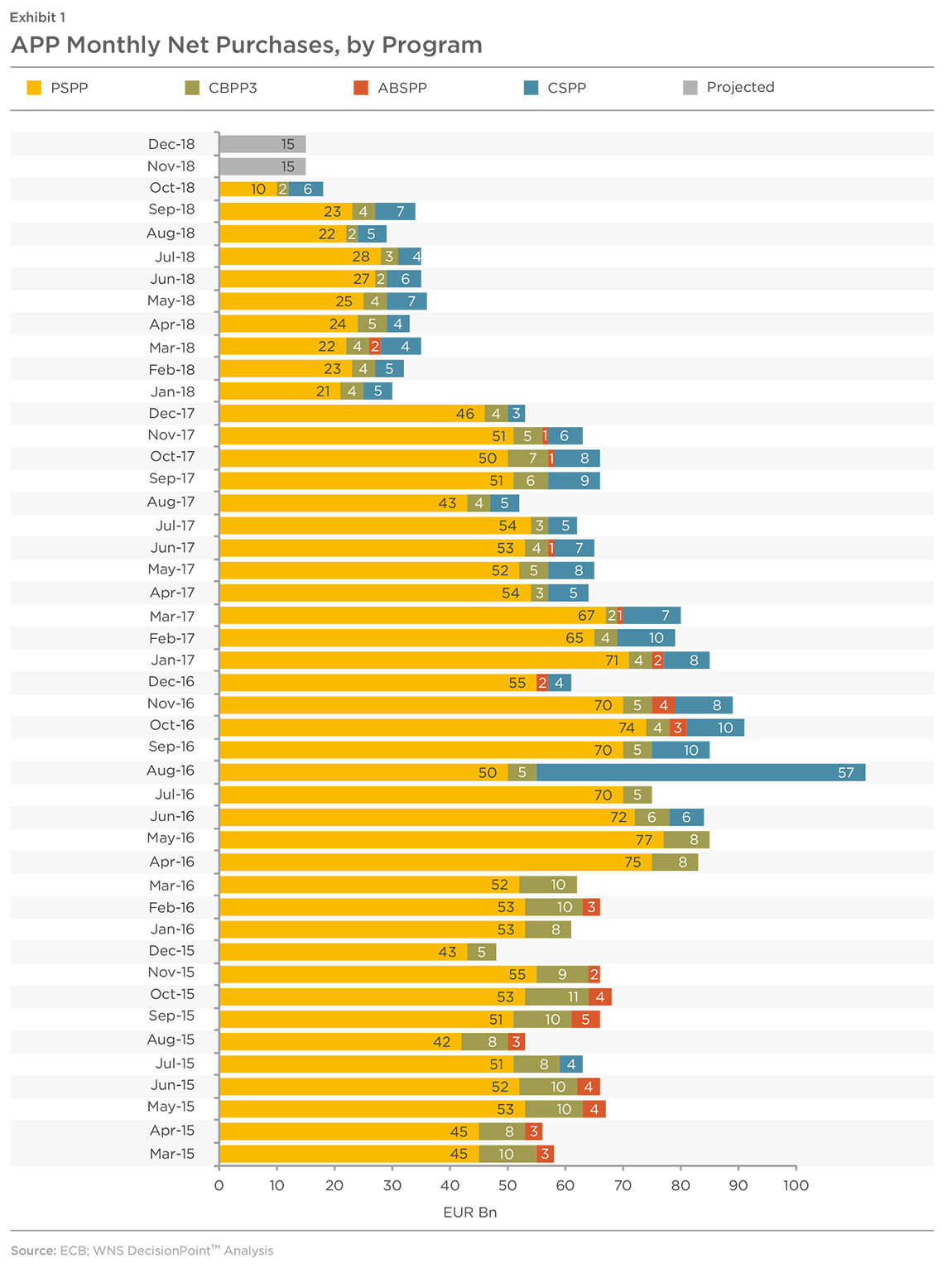

MONTHLY PURCHASES UNDER THE APP

The expanded APP includes all

purchase programs under which private and public sector securities are purchased by the central banks to address the risks of low inflation. Monthly net purchases of public and private sector currently equal EUR 30 Billion.4 On June 14, 2018, the Governing Council of the ECB stated that the monthly pace of net asset purchases will be gradually reduced to EUR 15 Billion by the end of December 2018, subject to incoming data confirming the medium-term inflation outlook. 5

ASSET PURCHASE PROGRAM HOLDINGS

Purchases of marketable debt instruments increase the Eurosystem holdings of such instruments and drive liquidity in the system.

IMPACT OF QUANTITATIVE EASING ON THE ECB'S BALANCE SHEET

In 2017, the ECB's total assets increased to EUR 414.2 Billion, primarily owing to its share of purchase of securities under the APP. These purchases resulted in an increase in the item 'Securities held for monetary policy purposes'.

Euro-denominated securities held

for monetary policy purposes accounted for 55 percent of the ECB's total assets at the end of 2017.6 Under this balance sheet position, the ECB holds securities under the Securities Markets Program (SMP), the three covered bond purchase programs (CBPP1, CBPP2 and CBPP3), the ABSPP and the PSPP.7 In 2017, purchases of securities under the CBPP38 , ABSPP and PSPP continued on the Governing Council's decisions on the overall monthly Eurosystem purchases.

In 2017, the portfolio of securities

held for monetary policy purposes by the ECB swelled to EUR 228.4 Billion as a result of the purchases, with PSPP purchases accounting for the majority of this increase. The decline in holdings under CBPP1, CBPP2 and SMP was due to redemptions, which amounted to EUR 1.5 Billion.

ASSESSING THE IMPACT OF QUANTITATIVE EASING ON BANK PROFITABILITY IN THE EURO AREA

The bond term spread, the difference between the short and long-term bond yields, is essential to bank profitability as banks engage in maturity transformation. Term spreads fell from very high levels during 2013 and 2014, but increased at the start of the Quantitative Easing (QE) program in 2015.

Term spreads started to decline after the ECB announcement of the expansion of the PSPP and the March 2016 decision to include corporate bonds. However, they increased again in the latter half of 2016 and toward mid-2018, when the ECB announced its decision to gradually reduce its asset purchases to half the current amount and eventually end the program.

Profits are affected when the lending-deposit rate narrows, as banks borrow short term, mainly through deposits, to invest in long-term assets. The lending-deposit rate, and hence the margin for banks to make profits, continues to drop. For the euro area as a whole, this reduction is visible for new lending to households and non-financial corporate sector. In terms of new lending, the lending-deposit spread in September 2018 was 1.37 percent for non-financial corporations and 1.82 percent for households.

PERCEPTION AND FACTS ABOUT BANK PROFITABILITY

The assessment till now implies that the total effects of QE on bank profitability are threefold:

- Positive effect: Scarcity effect by way of increase in capital gains;

- Negative effect: Lowering and flattening of the yield curve leads to declining profits generated from the lending-deposit rate spread;

- Improved macroeconomic

conditions strengthen the pace of credit offtake, thereby benefitting banks.

SO HOW DO BANKS PERCEIVE THE CURRENT SITUATION?

In its October 2018 survey, the ECB asked banks to take account of both the impact of asset purchases and impact of reinvestment of principal payments from maturing

securities under QE. Euro area banks reported that the APP had an overall negative impact on their profitability over the last

six months. A part of the decline in profitability was attributed to fall in the banks' net interest margins (net percentage of -31 percent, compared with -33 percent in April 2018), and the remaining proportion to capital gains/losses arising from the APP (-2 percent, compared with 3 percent in April 2018).9

With regard to capital positions, a

small percentage of banks reported that the APP had contributed to a decline in their capital ratios over the last six months, and they expect a neutral impact over the coming six months.

CLOSER ASSESSMENT OF BANK PROFITABILITY

Banks use deposits to finance their

loans. Since deposits are short term and loans are generated over the long term, banks rely on the term structure to generate profits. As observed before, the term spread has narrowed and so has the lending-deposit rate spread.

The ECB publishes aggregate

consolidated data on banks' balance sheets, profitability, asset quality, liquidity and solvency. Total profits, as well as those

indicators relating to operations and income-generating business, are the most pertinent indicators. We will examine two main

indicators:

- Total Profit Before Tax

- Operating Profit

Total Profit Before Tax is inclusive

of credit loss expenses and impairment losses on financial investment, as well as Operating Profit. Operating Profit has been broken down into its constituent parts, specifically net interest income (the main indicator for the lending-deposit spread), net

commission and fee income, operating expenses and a residual. The difference between operating profit and total profit (inclusive of credit loss provisions arising from bad debt) is indicative of the deteriorating credit quality that affected bank balance sheets during the crisis.

BANK PROFITABILITY, EURO AREA (AS A PERCENTAGE OF TOTAL ASSETS)

In the three graphs below, net

interest income and operating profits appear to be fairly stable across bank categories. Net interest income, which is a direct

indicator of the lending-deposit term spread, doesn't exhibit any volatility, a rather surprising observation under QE. There could be a couple of reasons for this. Firstly, the lending-deposit spread applied to new loans. Since loan

growth has been weak as a result of slow overall growth in the euro area economy, the rolling-over

of existing loans is severely impacted because of this. The low spread hence gradually feeds into the net interest income. Moreover, there is a possibility that banks have been compensating for the falling spread through fee

increases (loan origination fees and net of loan origination costs are recognized as interest).10 Secondly, banks have been able

to successfully generate profits

under QE.

Nonetheless, total profits have been volatile and at times, negative. Medium-sized banks have been the most severely hit. The main drivers of this volatility are losses arising from provisioning of non-performing loans, which accounts for the difference between the two types of profits. For small-sized banks, this gap has been eliminated.