Overview

2016 will witness the first set of live implementations of NDC (New Distribution Capability), proposed by the IATA1 in October, 2012. Over the last few years, NDC has been the source of quite a few disagreements between the IATA and the GDS2 companies. The various other key stakeholders in the adoption of this new standard are airlines, filing agencies3, travel agencies, IT providers, and travelers. There was an initial perception that the traditional intermediary role of the GDS in the airline distribution system will lose relevance as NDC will allow resellers to directly connect with the airlines’ offer management systems. However, over time and through a series of deliberations, GDSs have adopted a more conciliatory tone. They have accepted the initiative as an important one and are today, an integral part of the NDC implementation process. The future success of GDSs will be measured by how well they create products and solutions that embrace and take advantage of NDC and how fully they can exploit their future roles of aggregators in the new system.

NDC will allow airlines to combine relevant ancillary services and offer them with the base ticket, uniformly across all channels at competitive price points.

What Does NDC Plan To Achieve?

NDC is a program launched by the IATA for the development and market adoption of a new, XML- based data transmission standard (NDC Standard). The objective is to enhance the communication capability between airlines and travel agents. In effect, it aims to transform the way air products are sold to end-customers by ensuring that uniform and comprehensive merchandise information is made easily available across all booking channels. NDC will also be open to third-party intermediaries, IT providers and non-IATA members to implement and use.

With online shopping becoming more popular by the day, having all ticket options and ancillary combinations available through any channel is becoming a necessity. The industry’s current distribution system, with GDS as an intermediary, fails to meet this necessity. As a result, there is a commoditization of airline tickets. In an environment where other differences cannot be consistently seen, price has become the only consideration. NDC will allow airlines to combine various ancillary services, based on the customer’s preferences, and offer them with the base ticket at competitive price points. This will enhance the potential revenue from each passenger and omit the GDS cost per transaction in case the resellers connect directly with the airline offer management system.

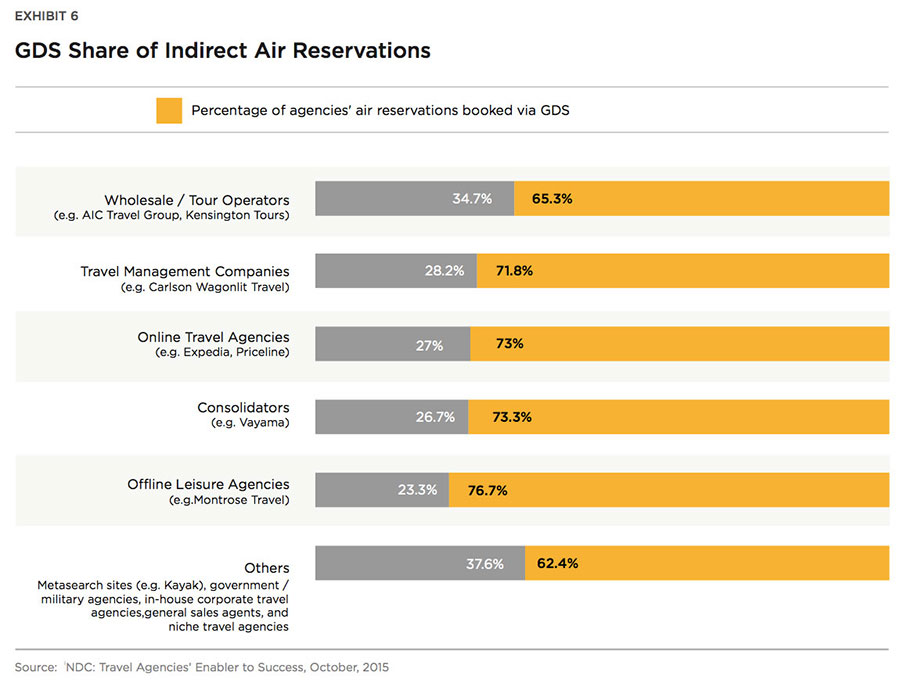

Exhibit 1 shows how a vast majority of the agencies feel they are at a disadvantage while selling airline ancillary products via GDS. The reason is evident in the following exhibit 2.

In addition to the above changes, NDC will also enable customization of offers by airlines, based on passengers’ buying history, if they choose to reveal their identity at the search stage. The new system, with consistent customer experience across channels, could change the approach from mere distribution to e-commerce.

To understand the flow of data at the backend that will make the above change a reality, it makes sense to have a look at the current flight distribution system and the planned distribution system post NDC.

How Will NDC Affect GDSs?

In the post-NDC implementation phase, all the merchandise content using the common XML data transmission standard will be available from the Airline Offer Management System rather than them being acquired separately from multiple sources such as ATPCO (Airline Tariff Publishing Company), OAG and Innovata (airline schedules database providers), and others. Agencies can, therefore, choose whether or not to directly connect to the Airline Offer Management System instead of connecting via GDS. However, given the level of competition among airlines to capture the market and the fact that GDSs’ share of global airline reservation volume is still quite significant, it is unlikely that the distribution systems will do away with GDSs.

There are, however, efforts to weaken GDSs’ influence. The Lufthansa Group started levying a GDS surcharge of €16 on every booking made via GDS, much to the resentment of the latter. The European Travel Agents Association, the European Tour Operators Association and the European Technology and Travel Services Association filed complaints against this move with the European Commission. The extent of impact of this development remains to be seen. According to figures released by the GTMC4, Lufthansa lost 8.5ii per cent market share (32.9 per cent to 24.4 per cent) between June and November 2015, after it introduced the GDS surcharge in September, 2015. GTMC stated that the drop indicates a shift of travel management companies away from Lufthansa to avoid passing on the charge to their customers. It should be noted that Lufthansa claims that this was due to cancellations of flights on account of a couple of industrial actions during this period, along with the fact that bookings increased through other channels such as LH.com.

The situation surrounding NDC adoption is being monitored by the airlines. According to IATA, 180iii airlines were asked in February 2016 if they would implement the NDC standard. 50 per cent responded saying they had plans within the next four years. The planned NDC adoption roadmap, created by IATA, ends in 2017.

What we can expect is the existence of a dual system in the coming years, with the following three segments:

- Airlines fully adopting NDC

- Airlines partially adopting NDC (not all schemas)

- Airlines not using NDC

A natural fallout of such a trend will be that GDSs’ role as intermediaries between airlines and agents will lose some importance and they will be more involved as aggregators and IT service providers in the emerging system. A look at the annual revenue of two of the biggest GDSs (Amadeus and Sabre) tells us how the revenue share of the distribution segment has already dropped in the last five years. This share is expected to dip further in the coming years due to their growing focus on the non- distribution part of their product portfolio.

Are GDSs Equipped To Face This Change?

The answer to this question lies in the way GDSs have evolved and diversified over the last couple of decades.

Since the late 1990s, GDS players have acquired other companies across the travel industry value chain, spanning ticket distribution, airline operations, airport technology, e-commerce travel platforms, hotel distribution, reservations and marketing. As the online marketplace grew rapidly, they kept acquiring companies offering specialized products in various geographies. Keeping in mind the evolving, lucrative travel and technology market, it was a safer bet to cast the net wide and try to develop a wider breadth of services than choose a specific line (if they could afford to).

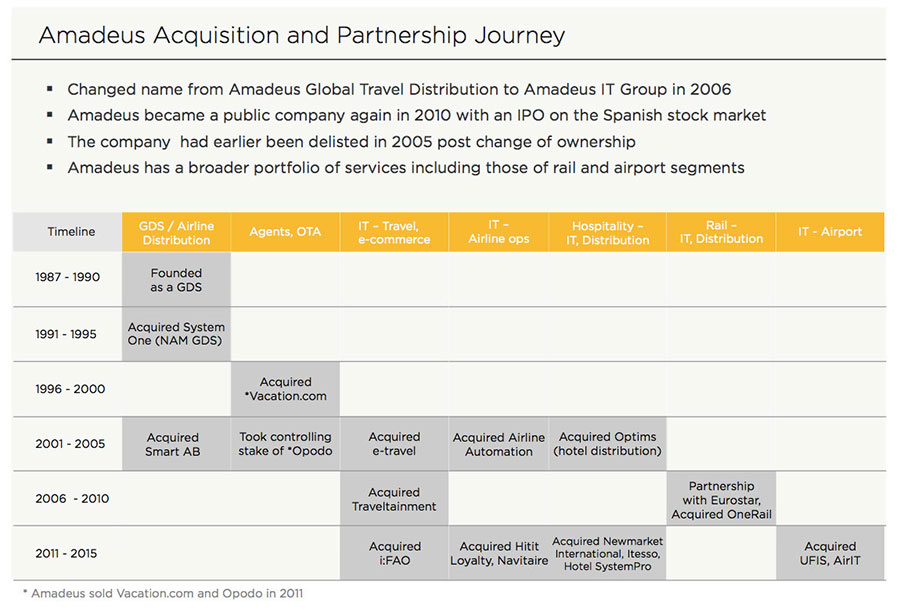

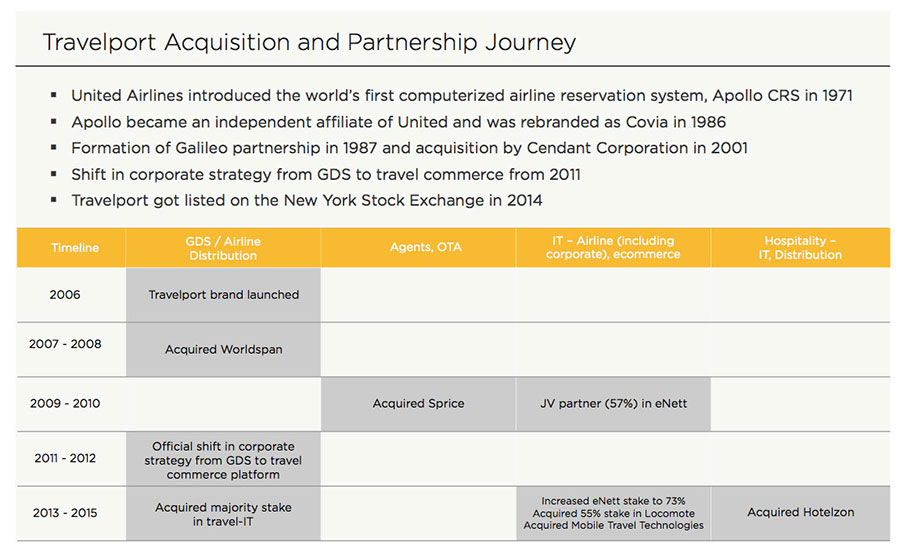

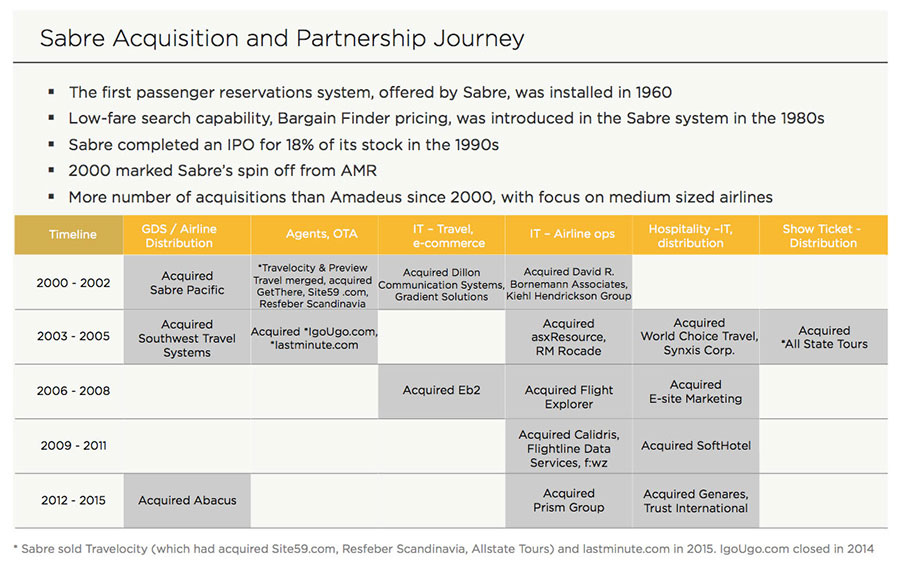

Effectively, this strategy resulted in GDSs’ rapid diversification into other segments of the broader travel and hospitality technology industry. Companies such as Amadeus and Sabre (which acquired Optims, Newmarket International, World Choice Travel, and SynXis) could develop expertise in the hotel technology platforms. In fact, Amadeus changed its name to Amadeus IT Group in 2006 to better reflect the expanded product portfolio. Acquisitions and partnerships were also extended to include operators in rail, car rental services, tourism, cruise and insurance. So, today, we have GDS companies which function as a conglomerate in the travel technology industry. What is interesting is that the two major GDSs – Amadeus and Sabre – have sold their stake in online travel agency (OTA) businesses over the last few years and have fully exited that segment. As the industry matures, we might see more of such sell offs and acquisitions until the time when GDSs are convinced of having a portfolio of services/products in line with a sustainable long-term strategy. At the moment, they have consolidated their interests into distribution and IT services for the travel industry.

As aggregators and technology service providers in the new scheme of things, GDSs will no longer enjoy the high barrier to entry that is in place in the current distribution eco-system. As such, they will face competition from newer players, who will now be free to enter the market, using the XML data standard open for all to use. Additionally, the IATA has partnered with Travel Capitalist Ventures to create the NDC Innovation Fund (NDCIF), in order to encourage the NDC enabling companies and take equity stake in select start-ups. However, 18 months on, Travel Capitalist Ventures has decided to leave the initiative, citing severely deteriorating global economic and market conditions, affecting the early stage investments. No investments have been made by the NDCIF to date. The IATA is still looking for a new investment partner for the innovation fund initiative.

It is critical that the GDSs constantly innovate and maintain a comprehensive and relevant range of offers. This can be managed through a two-pronged strategy consisting of:

- In-house development of new products

- Strategic acquisitions

In the above context, it is very important for each GDS to have a clear view of its relative competitive position against the peers in the industry.

What Does A Post-Ndc World Look Like?

Successful implementation of NDC will have unique implications for each of the stakeholders in the value chain. A holistic view of the implications is very important before one can draw any firm conclusions.

How each of the stakeholders respond and take advantage of the post NDC scenario, will be interesting to observe. The final process will generate a lot of structured customer data, enabling relevant customization of products and promotions.

What Should GDSs Be Doing?

Amalgamating the benefits offered by disparate units under a common GDS umbrella will be both a challenge and an opportunity. Smart GDS companies will embrace the challenges, innovate on product offerings and position themselves for the future. NDC is only one of the many ideas (sharing economy, meta-search engines etc.) that will use the open technology standard to further revolutionize the travel industry in the coming decade. GDSs must make it their goal to anticipate the upcoming changes and be prepared to deal with them. If GDSs can work to convert new players from competitors to collaborators, they can reap the benefits of building a fully connected, multi-modal travel eco- system. Given their already extensive influence, GDSs are in the best position to de-commoditize airline merchandise and further connect with the other members (hotel, restaurants, local transport) of the travel value chain. The ultimate goal of a GDS should be to morph itself into a one-stop travel platform.

NDC is challenging the core role of GDS as a distributor and pushing it to be an aggregator. The key is to create a comprehensive set of offerings that will facilitate partnerships by allowing seamless interaction with all the stakeholders of this interconnected industry eco-system. By doing this, GDSs can avoid becoming obsolete relics of the past, and instead, become champions of an innovative future.

References:

i. NDC: Travel Agencies’ Enabler to Success, October, 2015 - A report released by WTAAA ((World Travel Agents Associations Alliance), Atmosphere Research Group, T2Impact and IATA

iii. https://www.tnooz.com/article/half-of-airlines-will-move-to-ndc-and-agencies-love-it/